Resilience is no longer just about disaster response but a core measure of economic strength and investor confidence, Guyana’s Prime Minister Mark Phillips has told regional disaster managers.

Disaster management could no longer be seen as something activated only after an event, as that approach was inadequate for current realities, he declared. Resilience, he said, now sits at the centre of how countries are governed, shaping the economy, infrastructure, security and long-term development.

He said: “To govern well in this environment is to govern at the speed of risk, anticipating threats before they mature, investing ahead of need, coordinating across borders, and acting with resolve when the moment demands it. The windows in which decisions must be taken are narrowing, and the cost of acting late rises with every passing season. Approached in this way, resilience becomes a matter of competitiveness as much as protection.”

“A country that can keep its ports and its power running through a shock, and its public services available to those who depend on them, is one that investors trust and that its people can rely on. Equally, infrastructure built to withstand the hazards of a region retains its value over time. Early warning systems that reach every community lower the human and economic costs of an event. Further, the steady adoption of new technology from satellite data to improve forecasting gives governments more time to act before a threat becomes a crisis,” he said.

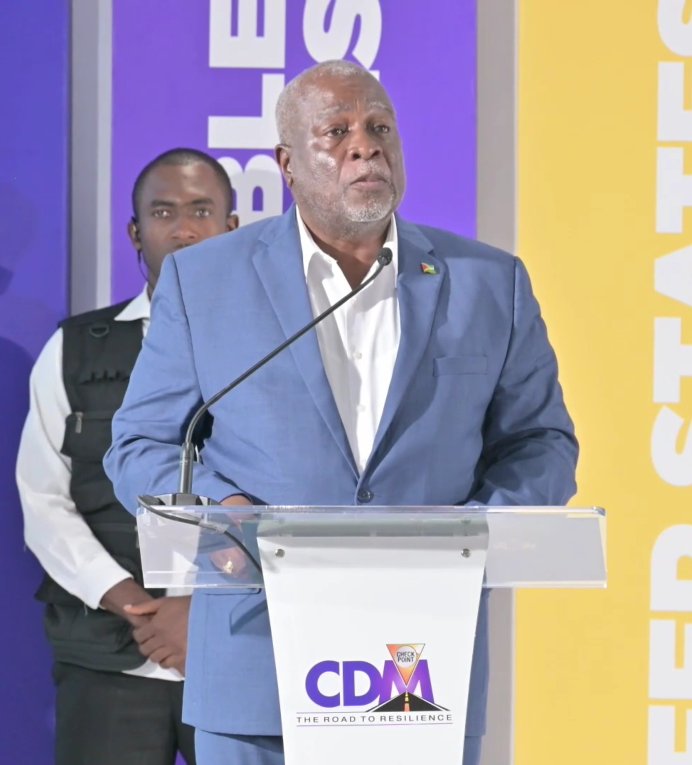

Phillips, a retired Brigadier of the Guyana Defence Force, was addressing regional leaders, development partners, private sector representatives, financial institutions and technical agencies at the official launch and partnership breakfast for the 14th Caribbean Conference on Comprehensive Disaster Management, an annual event aimed at advancing dialogue and partnerships on resilience, disaster risk reduction and sustainable development in the region.

He highlighted the need for regional cooperation, saying no country could secure resilience on its own and no single budget could finance it.

Adding that resilience capital did its “greatest work when it is well prepared in advance of disaster”, he said countries respond and recover faster when regional risk pooling and pre-arranged financing are in place.

The event, being held in Guyana, precedes that country’s hosting of the Caribbean Disaster Management Conference (CDM 14) in December, organised by the Caribbean Disaster Emergency Management Agency (CDEMA).

CDEMA executive director Elizabeth Riley said that while the Caribbean remains on the front line of a climate crisis it did not create, geopolitical uncertainty, supply chain disruptions, technological change, and growing competition for development financing are reshaping the environment in which regional governments and institutions operate.

Elizabeth Riley. (Photo Credit: Jenique Blegrave/Barbados TODAY)

“This really requires us to think differently about resilience and also to promote self-reliance. Resilience must be understood as a strategic governance development and economic imperative. It must shape how we plan, invest, and govern. This is especially important as development financing becomes more constrained and official development assistance declines. Maximising available resources, strengthening disaster risk financing, and embedding resilience into investment decisions will be critical to safeguarded development gains.”

(JB)