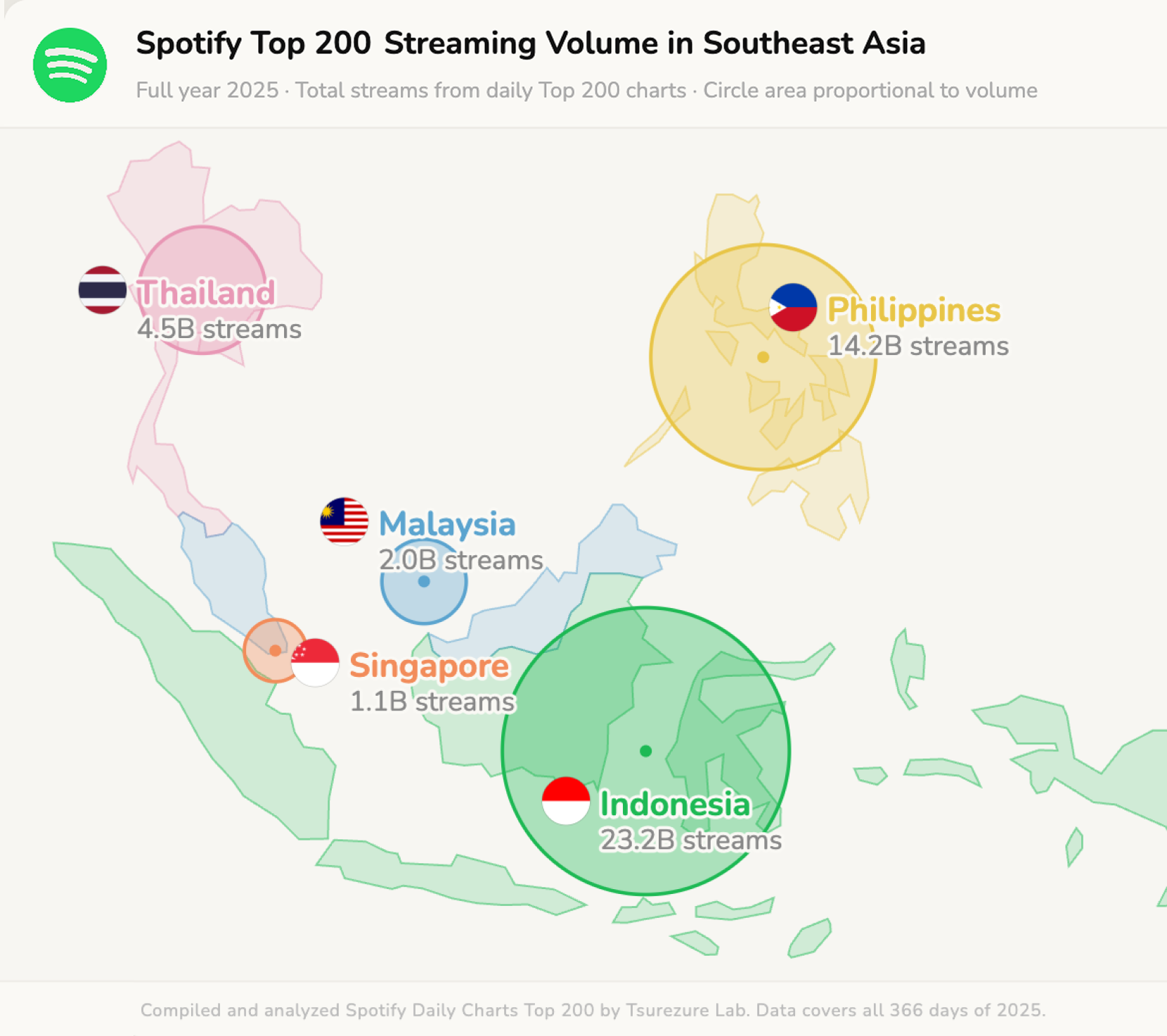

The scale becomes clear immediately. Indonesia alone generated 23.2 billion streams on the Spotify Top 200 in 2025 — more than double the Philippines’ 14.2 billion, and dwarfing Thailand, Malaysia and Singapore combined.

But raw volume is only part of the story. What Tsurezure’s genre-level analysis reveals is a consistent, three-year directional shift across the region: local music up, K-pop and Western pop down.

The five countries aren’t following the same playbook, with the data suggesting four distinct patterns of local takeover. The Philippines is a single-genre surge, with OPM (Original Pilipino Music, the umbrella term for Filipino popular music) claiming chart share almost point-for-point from Western pop. Thailand is a genre revolution, with K-pop’s collapse mirrored almost perfectly by the rise of T-Pop and Thai Hip-Hop. Malaysia and Singapore remain dependent on imported music but show early signs of internal change, with Indo Pop and Mandopop gaining ground in viral charts. And Indonesia — the region’s largest market by far — has built something more complex: a three-layer ecosystem where mainstream Indo Pop, independent singer-songwriters and a new wave of hipdut each run their own pipeline from discovery to daily listening.

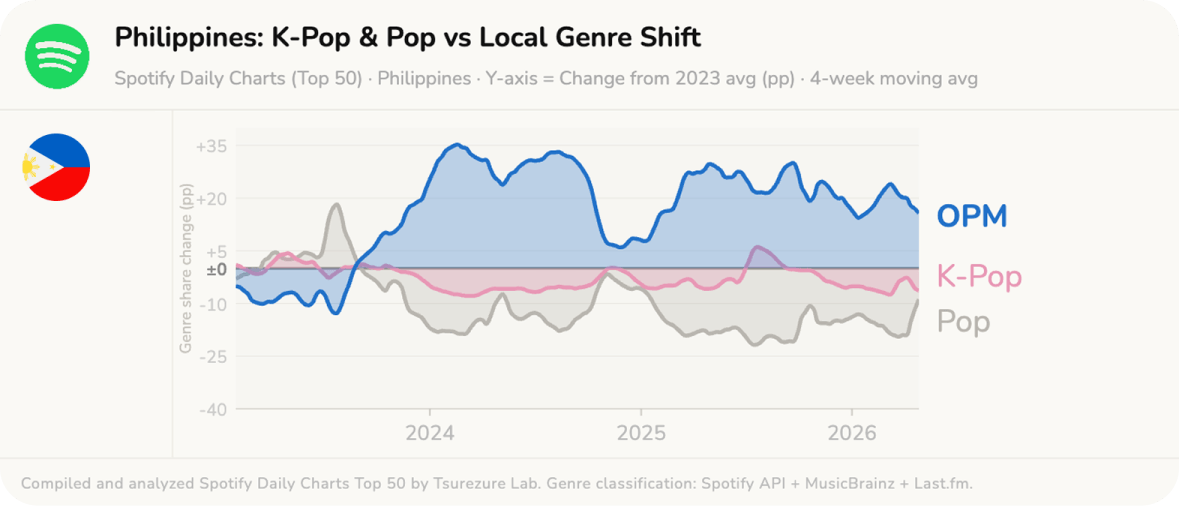

In the Philippines, the speed of the shift is striking. OPM’s share of the Spotify Top 50 jumped from 44 percent in 2023 to 69 percent in a single year — a 25-percentage-point surge unmatched by any of the other countries Tsurezure studied. Since then it has settled around 63 percent, suggesting the Philippines crossed a tipping point in 2024 and entered a new equilibrium.

OPM’s gain came almost entirely at Western pop’s expense — the correlation between the two is r = −0.903, a near-perfect inverse: for every chart position Western pop gave up, OPM claimed it.

Part of that surge can be traced to BINI, a Filipino girl group whose rise carries a particular irony: built on the K-pop idol training model, BINI is now outperforming K-pop on its own home charts. By staying true to its P-pop roots, BINI built a global following that culminated in a Coachella performance in April, making them the first all-Filipino girl group to play the festival.

The Philippine newspaper BusinessMirror reported that the group drew some 125,000 people to its two weekend performances, the first of which has amassed more than 27 million views online, second only to Justin Bieber. Post-Coachella, BINI announced the Signals World Tour 2026, covering the United States, Canada, the United Kingdom and selected European countries.

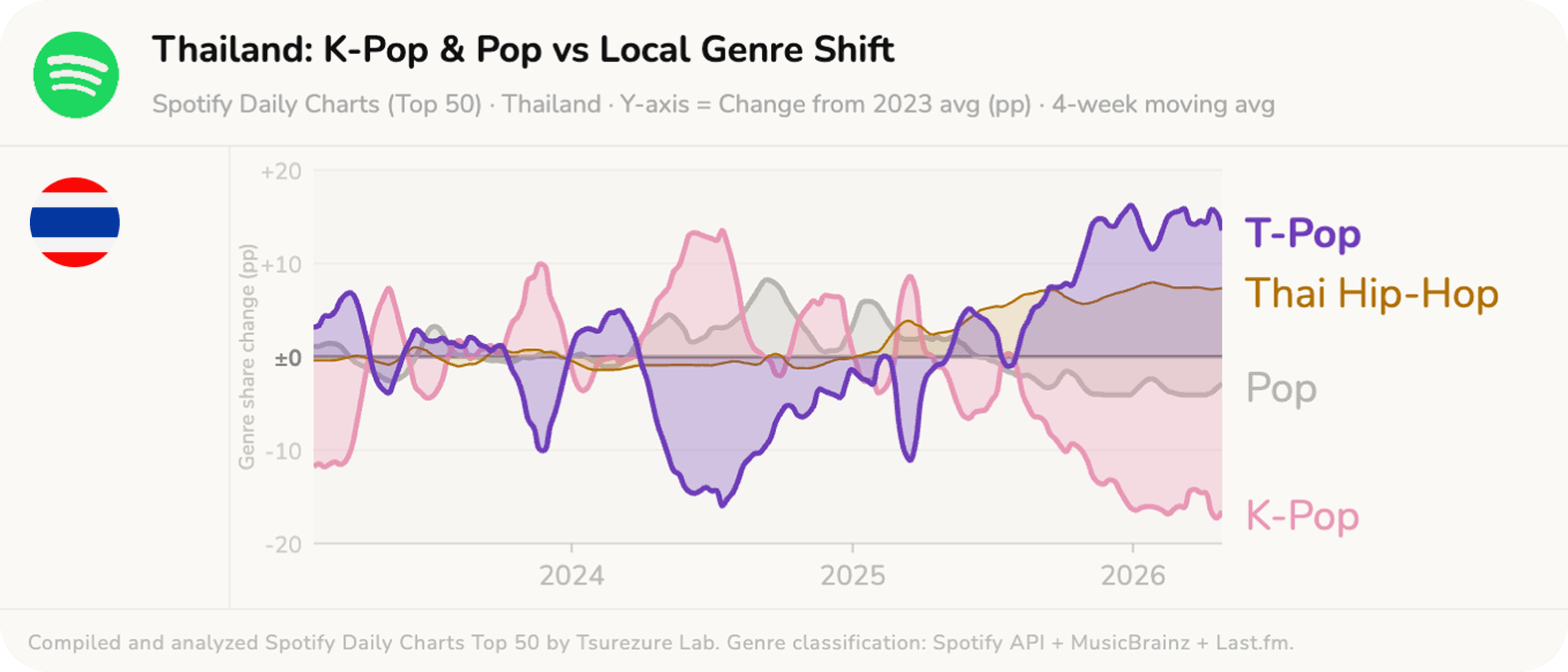

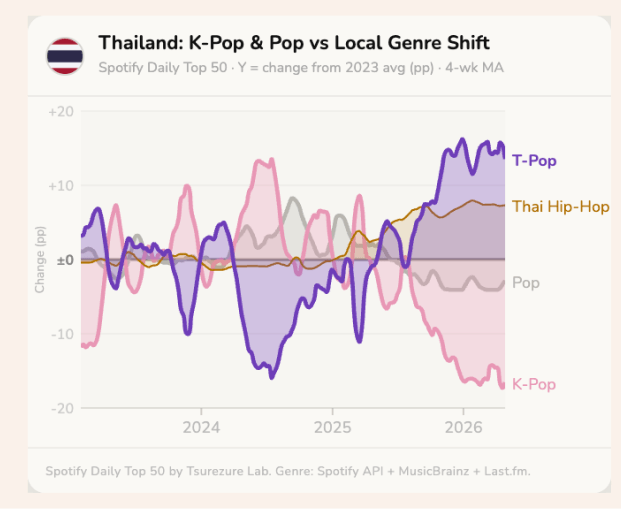

In Thailand, the shift has been the most dramatic of all five markets — and the most structurally interesting. T-pop’s share climbed from roughly 65 percent to 78 percent between 2023 and 2026, while K-pop collapsed from 27 percent to 11 percent, the steepest decline among the five countries. The correlation coefficient of -0.931 is also a near-perfect inverse: chart positions didn’t just shift, they were exchanged.

What makes Thailand unusual is that K-pop’s exit was a two-pronged replacement. T-Pop absorbed one portion of its former audience while Thai Hip-Hop captured another — rising from virtually absent in 2023 at 1.4 percent to 8.9 percent by 2026. Milli, Youngohm, URBOYTJ and F.Hero filled the space K-pop left behind. Two local genres rose in tandem rather than competing.

Thai pop singer Jeff Satur’s sold-out Red Giant Tour across South America and Asia in 2025 confirms T-pop’s growing international reach, with Forbes even featuring him as the first T-pop artist to have his music showcased at the Grammy Museum.

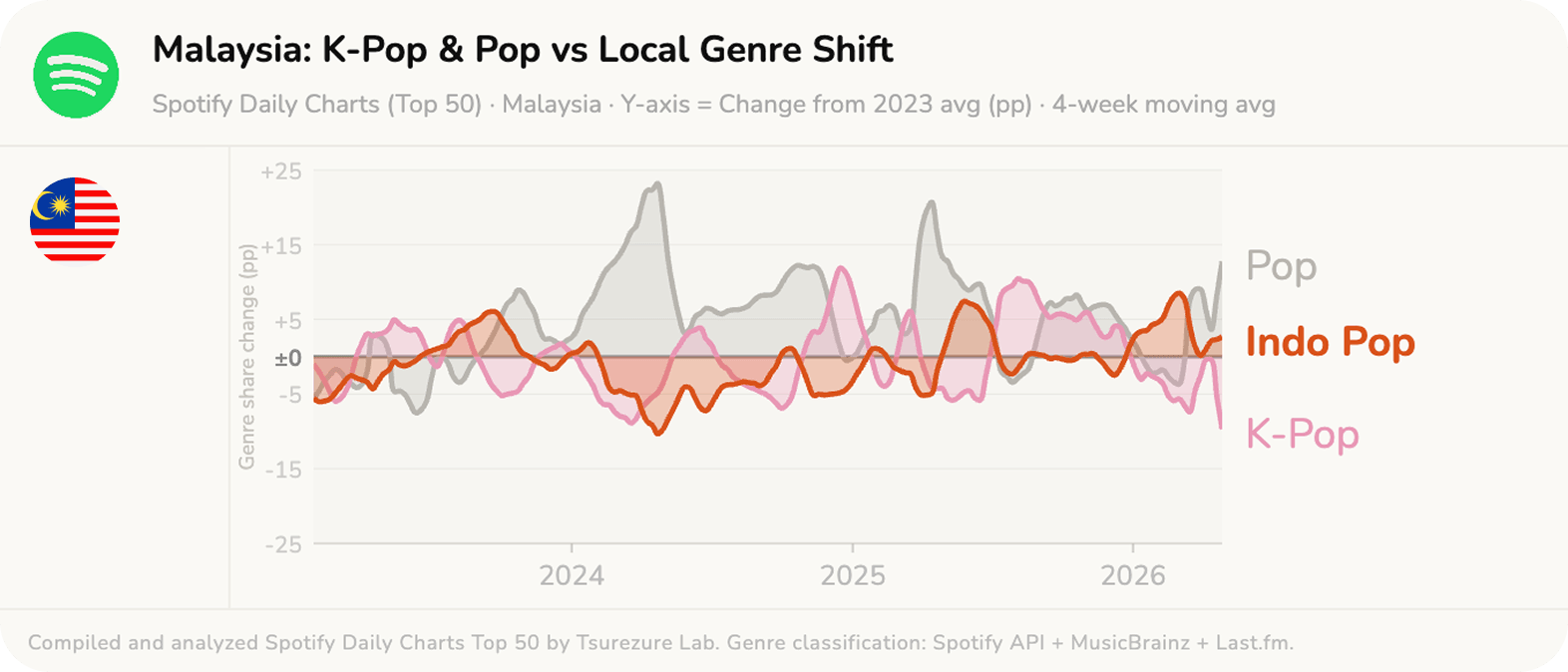

Malaysia tells the most unexpected story of the five. The “local” genre gaining ground there isn’t Malay pop — it’s Indonesian.

The linguistic and cultural proximity between the two countries has helped artists like Bernadya and Juicy Luicy build real audiences across the border, with Tenxi, Jemsii and Naykilla’s “Garam & Madu (Sakit Dadaku),” meaning Salt & Honey (My Heart Aches), charting strongly in Kuala Lumpur.

The cross-border flow is accelerating faster than it might appear. Tsurezure has also conducted genre-level analysis that reveals a striking trajectory for dangdut-influenced music from Indonesia. It barely registered on the Malaysian Top 50 in 2023, at less than 1 percent. By 2025 it had jumped to 5.9 percent; by early 2026, 7.1 percent — a trajectory that lines up precisely with the TikTok-driven explosion of hipdut acts like Tenxi and Naykilla in early 2025.

Of the five countries in this analysis, Indonesia is the only one whose homegrown genre has established a measurable, sustained presence in another country’s daily charts. In streaming terms, it is Southeast Asia’s sole cultural exporter.

One other detail worth noting: classic Western pop continues to hold its ground in Malaysia in a way it doesn’t elsewhere, with songs like One Direction’s “Night Changes” (2014) and Charlie Puth and Selena Gomez’s “We Don’t Talk Anymore” (2016) still appearing in regular rotation. Nostalgia, it seems, travels well.

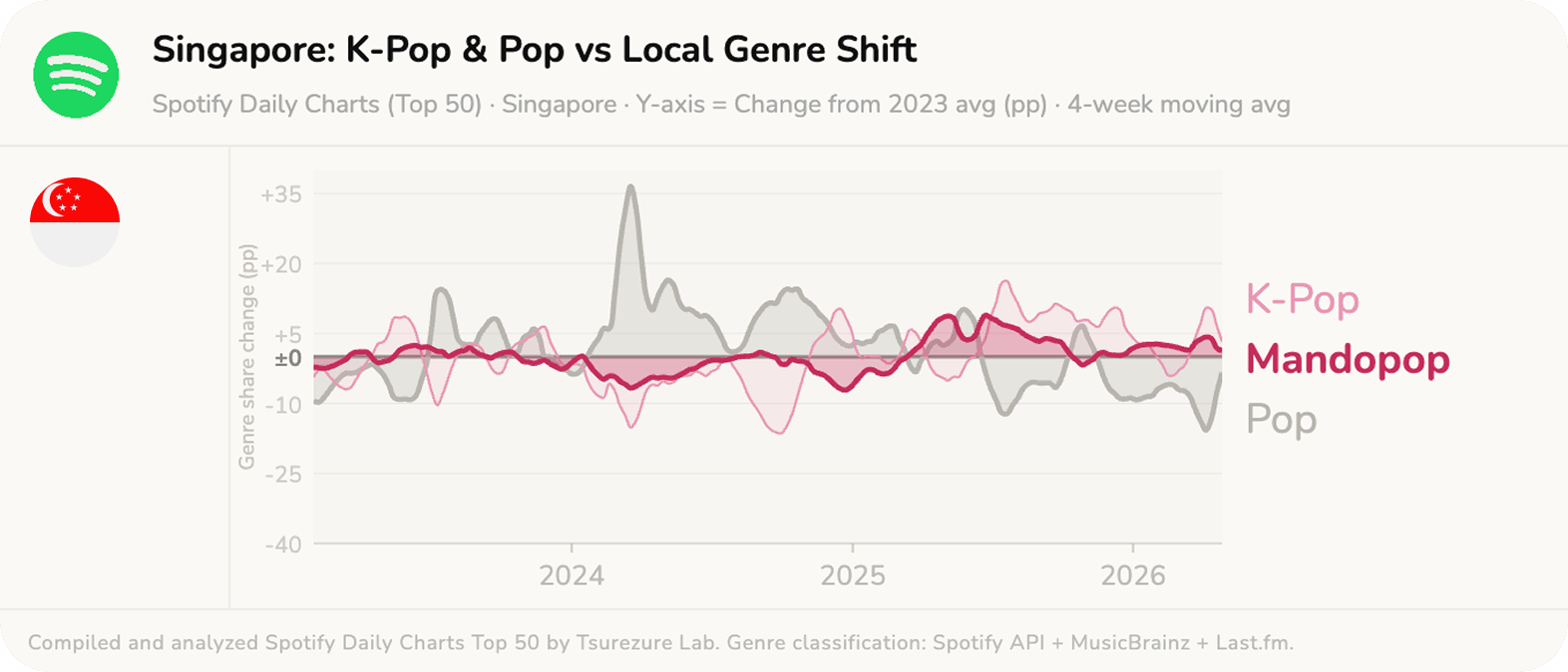

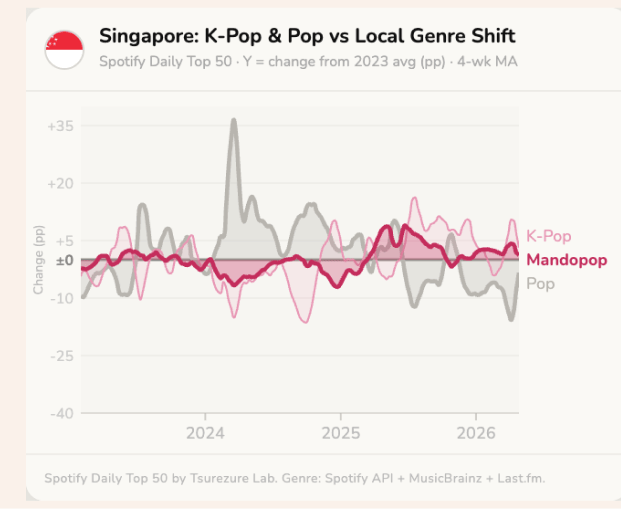

Singapore is the outlier. It’s the only market in this analysis where K-pop hasn’t declined — holding at around 31 to 33 percent of daily chart share since 2023, a level of entrenchment not seen elsewhere in the region. BTS members Jin, Jimin and Jung Kook and newly-launched group CORTIS continue to hold their ground alongside Western pop staples like Olivia Rodrigo.

But the more revealing signal lies in Spotify’s viral charts, which track discovery rather than habitual listening. Mandopop — represented by artists like LBI利比 and Silence Wang — currently accounts for 22 percent of Singapore’s viral chart, more than two and a half times its 8.4 percent daily share. That is the largest discovery-to-consumption gap of any genre across all five markets. If that viral energy converts to habitual listening, as it has elsewhere in the region, Mandopop could become a considerably larger force in Singapore within the next few years.

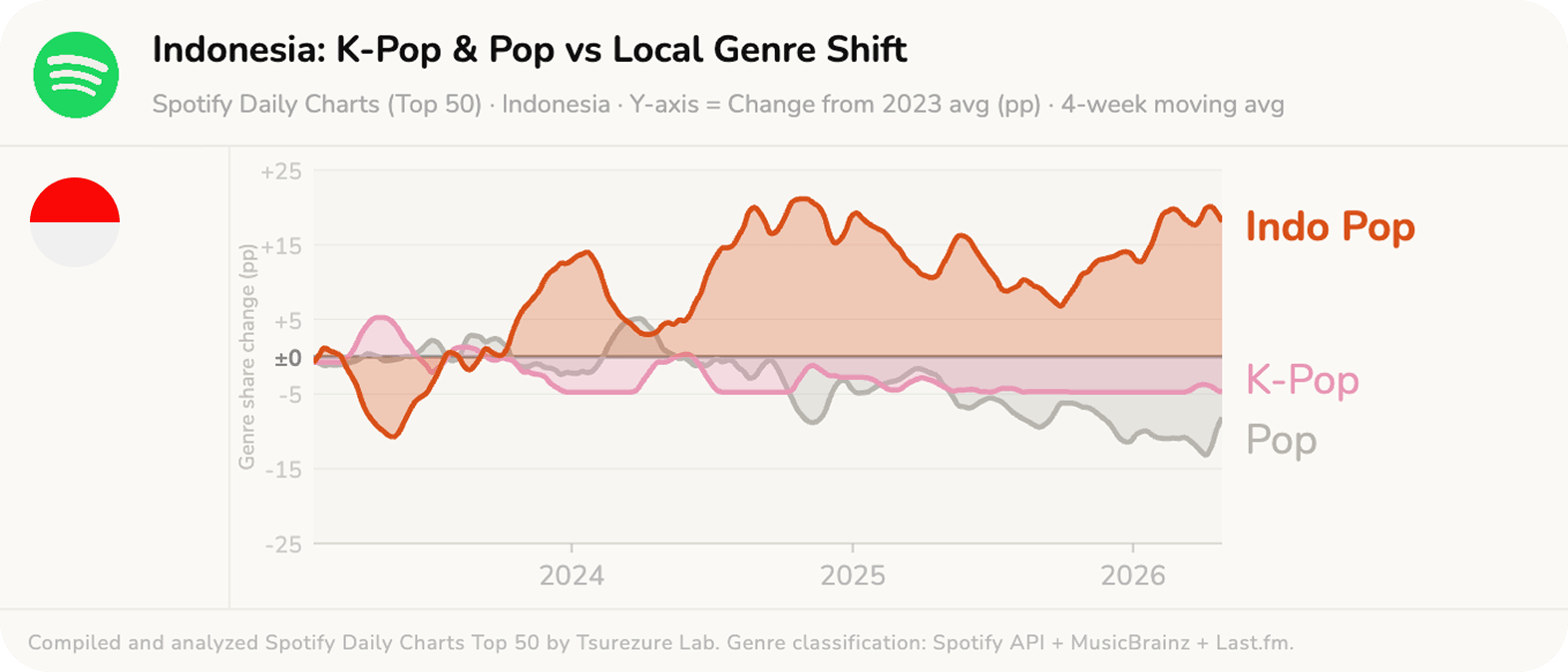

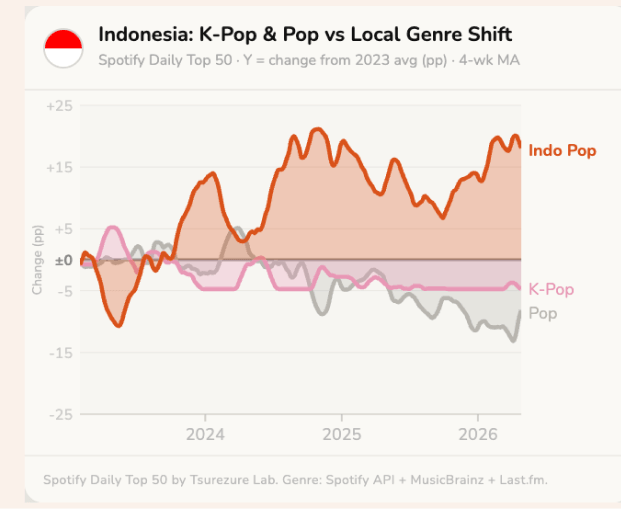

Of the five countries, Indonesia tells the most layered story — not a single surge or a genre swap, but a three-tier ecosystem running in parallel.

The first layer is mainstream Indo Pop: artists like Tulus, Raisa and Mahalini who command the majority of daily chart real estate. The second is the Indonesian indie scene, centered in Bandung and Jakarta — Bernadya, Sal Priadi, Nadhif Basalamah and Hindia, whose songs typically surface on viral charts before graduating to daily rotation. The third is hipdut, driven by Tenxi, Naykilla and Jemsii — the same artists who performed at Bengkel Hall.Each layer has its own discovery-to-consumption pipeline, and they coexist rather than compete.

The overall trajectory has been one of steady acceleration. Local genres held 62 percent of the daily Top 50 in 2023, jumped to 73 percent in 2024 — the year Bernadya and a wave of indie acts broke through simultaneously — and reached 82 percent by early 2026. Tsurezure’s genre-level analysis adds a further dimension. Indo Pop’s daily-to-viral gap is −41.6 percentage points, the largest of any local genre across all five markets: Indonesians aren’t “discovering” Indo Pop anymore. It is simply what they listen to.

In 2025, around Indonesia’s Independence Day on August 17, dangdut‘s share of the daily chart spiked to roughly 12.6 percent, about three times its usual level. No other country in this analysis shows anything comparable. Streaming, it turns out, mirrors the calendar of national identity.

K-pop, meanwhile, has entered what Tsurezure calls bifurcation — a pattern unique to Indonesia. Its daily chart presence has nearly vanished, falling to 1.3 percent, but it still accounts for 11.1 percent of the viral chart. New releases from acts affiliated with HYBE, the Korean conglomerate that grew from BTS’ original label, still spike in the viral rankings; they just no longer convert to sustained daily listening. The fandom’s discovery circuits are intact. What’s broken is the bridge to habitual consumption.