The pattern suggests more households are turning to credit sources that are easier to access and offer more flexible terms, amid tightening conditions in the formal system. That signals not only liquidity stress, but growing financial vulnerability—since some alternative credit sources may carry higher costs and greater long-term risks.

SCB EIC said the household debt problem is not occurring in isolation, but is linked to a broader set of pressures, particularly signs that the labour market is weakening.

Thailand’s unemployment rate in the first two months of 2026 rose to 0.9%, mainly because new graduates are finding it harder to secure jobs, pushing up unemployment among those who have never worked before.

In addition, employment among those aged 15-24 has continued to shrink for a second consecutive year, reflecting weaker labour demand. Some workers have therefore shifted into the informal sector, which may provide short-term income but offers less security and typically lower pay, reducing their ability to service debt.

The overall employment picture in 2025 also showed worrying signs, with total employment continuing to fall, especially in the industrial sector, which contracted for the first time in four years.

At the same time, some workers moved from agriculture to the service sector in search of higher incomes. However, the service sector has limited capacity to absorb labour, and many jobs remain low-paid. As a result, average incomes across the workforce have declined. Even where people remain employed, earnings are often insufficient to cover living costs.

Meanwhile, the continued decline in new business formation points to slowing private investment, limiting opportunities for job creation.

Rising living costs are another major pressure point. Higher energy prices linked to the Middle East situation have pushed up prices for goods and services more broadly.

EIC estimates that Thailand’s inflation this year will accelerate to 3.2%, putting further pressure on real wages. Higher costs are also squeezing businesses’ profitability, which could lead to reduced hiring or slower wage growth.

Sectors facing heavier cost pressure include rice farming, wood production, and the chemicals industry, employing around 2.6 million workers, or 6.5% of the total labour force.

Workers in these sectors face risks such as reduced working hours, fewer overtime payments, or delayed hiring, directly cutting income. When incomes fall while debt obligations remain, debt-servicing capacity weakens further and may lead to rising non-performing loans.

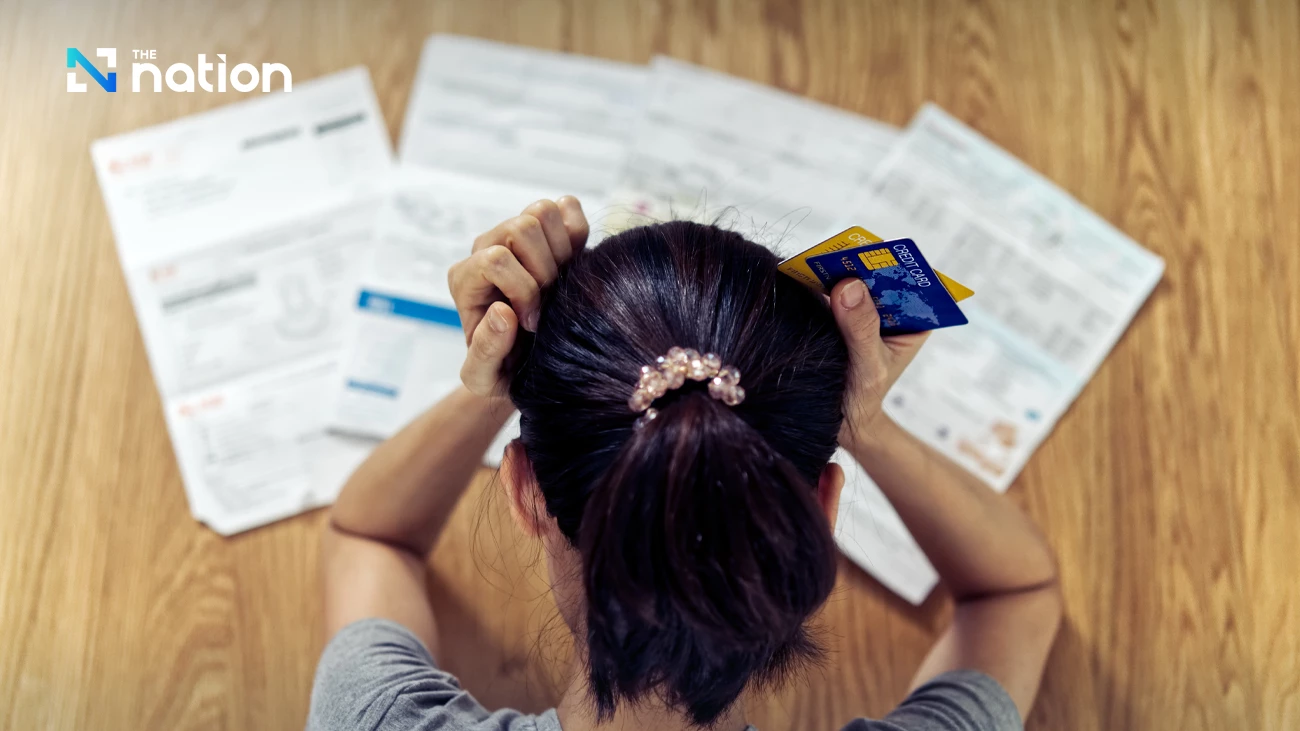

Overall, Thai households are facing mounting challenges as income falls, debt rises, and repayment becomes harder. If incomes do not recover, this cycle could intensify and raise broader risks to the economy.

In the short term, cost-of-living support, especially for energy, should be targeted to reduce household burdens. At the same time, debt restructuring can ease pressure on borrowers while incomes remain weak.

Over the longer term, solutions must focus on raising incomes through skills development, creating higher-productivity jobs, expanding economic opportunities, and strengthening the welfare system to help households cope with volatility.

Ultimately, Thailand’s household debt situation reflects risks driven not by a single factor, but by overlapping pressures: a fragile labour market, unstable income, and rising living costs. Without targeted solutions, these risks could eventually spread into a systemic economic problem.