As a child, Irit Shaulian thought that she would turn to the worlds of education and maybe psychology, but life had other plans, and she points out that she has been in the capital market for almost 30 years. She currently serves as a senior investment advisor at Propound Investment House, which manages approximately NIS 3.5 billion in investment portfolios, mutual funds, hedge funds and personally managed provident funds (IRA).

● The CEO who retired today with NIS 110 million in his pocket. At least

● 40 to 40 | From the heart of Silicon Valley to managing billions of investments in Israel

Shaulian has gained a lot of experience in the capital market, during the last 8 years at Propound and before that in the 20 years she worked at Biobank from the international group, which brought her into contact with all types of crises that the stock market can offer. In her current position, she determines the investment policy for the clients under her care, while weighing their preferences. According to her, “My fingers don’t do the actual trading. I provide ongoing advice throughout the life of the portfolio, and the investment manager implements the policy for the client.”

She also meets the old dreams in her current occupation, when “there is a lot of psychology in the investment world, and also emotion, which motivates us, and not always rationality. I can really identify which of the investors works from emotion and who works from rationale.”

Even after the flight of the local stock market in recent years, when the flagship Tel Aviv 35 index rose by over 75% in the past year, Shaulian repeats an important mantra, which justified itself in the sharp declines of March (and the jump that came immediately after): “If you don’t need the money, don’t do nonsense – don’t sell in a crisis, don’t set a loss, let the money work.”

According to her, “The market knows how to correct itself, and it doesn’t matter what you call this crisis. Unfortunately, we experienced not only financial crises (like in 2008), but also October 7th. It didn’t hurt the stock market that much, except for a very short period.” In her view today, “even in contrast to Corona, if we look at the last five years, the customers have matured.”

“It’s not right to enter the bunker”

In view of such a strong rise in the local stock market, when many of its stocks have provided triple-digit returns in recent years, and when the markets in Tel Aviv and the USA are once again breaking new records, one must ask whether it is worth taking the foot off the gas a little?

Shaulian thinks not. “It’s never right to go into a bunker, there are times when we really reduce equity exposure. There were times when we held more bonds or cash. At the moment we think there should be risk diversification, but not necessarily a reduction in equity position. The exposure between Israel and abroad within the equity part is also balanced today. This is after last year, after all the increases in the local market, we were 60%-40% in favor of Israel. Today Israel is more expensive, so we reduced it a bit.”

In the equity component, its exposure today is equal between the local market and the world. “The Israeli market was cheaper than the US for a long time. Today it is more expensive and more fully priced. That’s why there is no clear priority (for Israel),” says Shaulian. “This is why we returned to our historical levels of half-and-half.”

As for the solid channel, according to her, “In general, we have diverted some of the bonds in the shekel channel to index-linked bonds. We are roughly half-and-half between the shekel and the tight in this component.” The reason for increasing the tight component, which is intended to protect against rising prices (inflation), is that “the main parameter that drives the markets is inflation. Expectations for price increases in the markets are not very high at the moment, and perhaps they do not fully reflect all inflationary pressures.

“In Israel, the pressures on prices can stem from both rising energy prices and the expansion of the government deficit following the war,” she elaborates. “An increase in sea freight prices translates into an increase in commodity prices, food prices. We see that it affects the entire chain. That’s why we shortened the average life of the debt components in the investment portfolios. Today it is medium-low – around 3.6 years.”

She adds that “In light of the current uncertainty in the economy, it is possible that the Bank of Israel’s interest rate will decrease, but at a lower rate than we estimated in the past. The reductions will be less aggressive. The governor in the US is also moving away from the approach of lowering interest rates. At the same time, the strengthening of the shekel against the currencies of the world softens part of the jump in inflation. But as mentioned, on the other hand, we also see an increase in sea freight prices.”

Olyan believes that the strength of the Israeli economy is clearly evident in the conduct of the market: “The shekel has strengthened, the Israeli economy has worked almost without interruption to growth, and is on the whole at full employment. Those who are trying to recruit workers feel that there is a shortage.” In addition, according to her, the market is witnessing a massive influx of dollars into Israel, a flow that resulted from transactions in the high-tech industry, sales of the defense industries, as well as from the diversion of funds by Israeli investors back to Israel.

In the last year, the dollar has weakened by 20% against the shekel, and according to her, “Maybe it’s strange to say, but Israel is considered a little safer, and we see money coming in.”

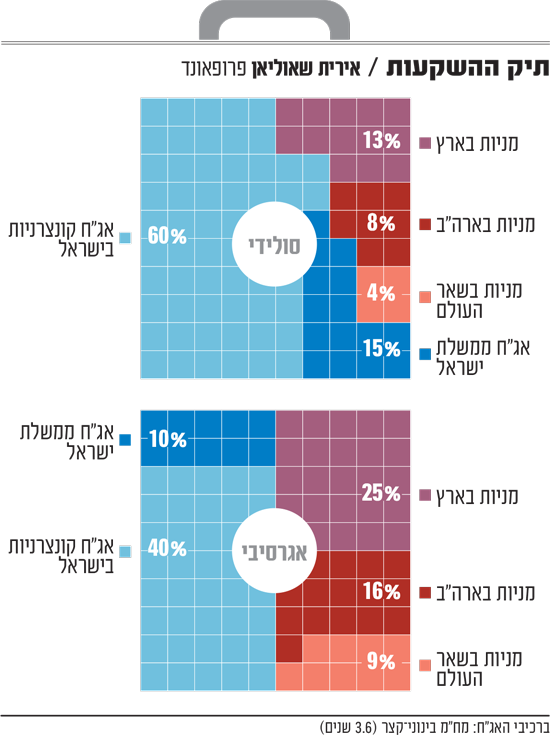

Shaulian’s solid investment portfolio, therefore, consists of 13% shares in Israel, 8% shares in the USA, 4% in shares of the rest of the world (mainly in Europe). The bond component consists of Israeli government bonds (15%) and Israeli corporations (60%) with a 3.5-year maturity. For an aggressive investor, it offers a portfolio of 25% shares in Israel, 16% in US shares and 9% in the rest of the world. 10% will be allocated to Israeli government bonds and the remaining 40% to Israeli corporate bonds.

Recommended sectors

in Israel

banks

renewable energy

infrastructures

retailing

stay away in the short term

Residential real estate

Insurance

abroad

The big indexes

USA – S&P, Nasdaq

Europe – Eurostox

Banks and renewable energy

Meanwhile, Profund has preferred sectors: “Primarily the banks, which have been profitable and stable over the years. The shares are relatively cheap compared to the market and they also pay dividends. We specifically prefer the larger bank shares, and the sector in general.”

According to her, another area is the renewable energy stocks, which yielded dream returns for investors in the past year, sometimes of hundreds of percent. “This is another sector that we really like. Electricity prices are rising, the demand for energy has increased due to the introduction of AI, which requires the establishment of server farms (data centers), which increases the demand for electricity. To catch up with the demand for energy, only traditional energy companies (conventional power plants) will not be enough. In our estimation, the renewable energy companies are expected to double and triple themselves in the next three years, after the raw materials of which have been discounted – panels, batteries (for energy storage), etc.

code of ethics

appearing

in the trust report

according to which we act. Expressions of violence, racism, incitement or any other inappropriate discourse are filtered out automatically and will not be published on the website.