June 7, 2026 11:19 am

Today marks 100 days since the start of the war in the Middle East, and the conflict continues to cause significant volatility in stock, bond, currency and commodity markets and in all regions of the world, while a lasting peace agreement remains elusive, writes CNBC.

Negotiations between the US and Iran have stalled, with Washington and Tehran sending mixed messages about the state of peace talks, while both sides occasionally exchange military strikes. However, a fragile truce remains in place to allow diplomacy.

As the conflict continues, the pressure on certain economies and parts of the financial markets is increasing.

Wall Street bulls ignore the war

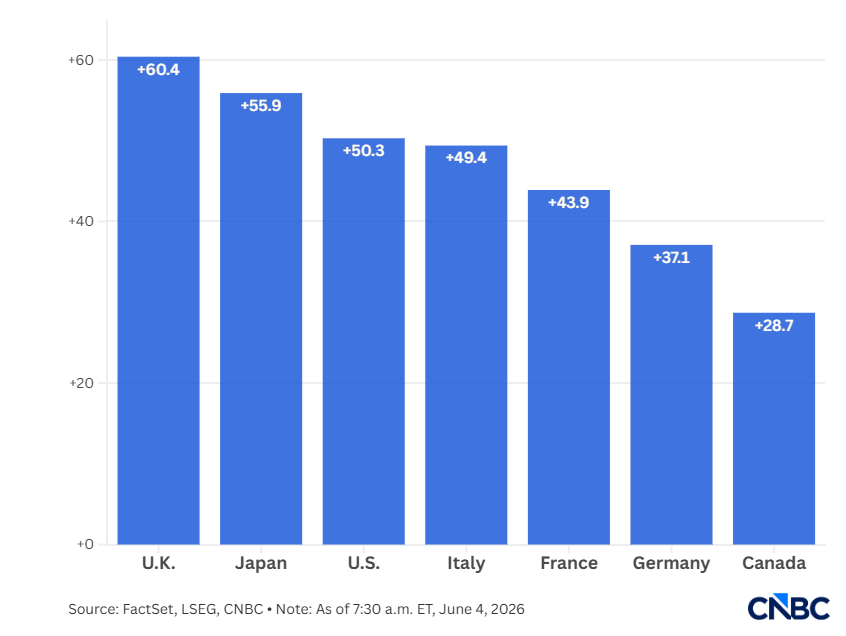

Immediately after the first US and Israeli strikes on Iran, stocks around the world fell. While stocks in some markets have struggled to regain momentum, Wall Street’s main indexes have recouped initial losses as investors look past the war, higher oil prices and the impact of the conflict on inflation. The S&P 500 hit new all-time highs even as the war continues.

Iain Barnes, chief investment officer at Netwealth, said that stock markets were dominated by assumptions that the war would shift major energy-importing economies from a “mild disinflationary environment” to a stagflationary one. However, optimism about the future disruptive power of artificial intelligence and the profitable environment for American companies also came into focus.

“That pushed equity markets higher, but clearly led by companies in the US and Asian markets that are seen as direct beneficiaries of AI spending,” he said in an email. “European stocks were more muted as the impact of rising energy costs is more problematic.”

“Spending on AI infrastructure has pointed to a number of potential bottlenecks, primarily the insatiable demand for computing capacity that is fueling semiconductor stock price growth,” Tony Meadows, head of investments at BRI Wealth Management, told CNBC in an email.

“Markets and entire economies like South Korea and Taiwan are getting better growth forecasts as a result.”

He added that the US, being largely energy self-sufficient when it comes to oil, does not feel the pressure caused by the Gulf conflict as directly as other economies.

“If the Strait of Hormuz remains closed, inflation is likely to rise, but investors seem ready to believe that neither Trump nor the Iranians want to prolong this conflict,” Meadows added. “However, at some point the impact of the conflict, if not resolved, will lead to a drop in demand that investors will not be able to ignore. But that point has not yet been reached and, while few stocks lead the markets, positive news for those companies outweighs uncertainty in other sectors, such as consumer stocks.”

Bond yields soared

Government bonds have been volatile since the outbreak of war, but yields on sovereign debt remain high.

Bond yields and prices move in opposite directions, so high yields mean that there is still downward pressure on the value of these assets.

Yields on US government bonds are among those that have jumped since the start of the war, as investors have rushed to factor in higher inflation and tighter monetary policy. Last month, the yield on the 30-year US bond reached its highest level since before the financial crisis.

A similar pattern was observed in many major economies.

The United Kingdom, which is simultaneously caught up in domestic political turmoil, has seen a particularly strong sell-off in government bonds, known as gilts.

Neil Birrell, chief investment officer at Premier Mitton Investors, told CNBC that bond markets have taken the view that there is “something real to worry about,” pointing to fears of higher inflation, weaker growth and supply chain disruptions.

Oil prices have calmed, but concerns remain

The Strait of Hormuz, a key oil shipping route in the Middle East, was essentially closed for the duration of the war, leading to large swings in oil prices as traders reacted to news of missile attacks, peace talks and ceasefires.

Although prices have fallen significantly from their wartime highs, they are still far higher than before the start of the conflict. The global reference Brent oil futures are trading around 36 percent above the pre-war price, while the American West Texas Intermediate futures are still up almost 50 percent.

The blockade of the Strait of Hormuz, along with the damage and shutdown of key energy production facilities in the Middle East, has created severe supply constraints.

Supply problems have forced oil importers to look for alternative suppliers. In the past 100 days, US crude oil exports have increased, which Tamas Varga, an analyst at PVM Oil Associates, described as one of the “obvious mitigating factors preventing significant price growth” in crude oil markets.

“These include the release of strategic oil reserves, exemptions from sanctions for Iranian and Russian oil already offshore, reduced Chinese oil imports, alternative routes to transport oil from the Persian Gulf to Asia and Europe, increased US exports of crude oil and derivatives and, finally, a drop in demand,” he said.

However, he added that if oil stocks continue to decline during June, they will reach critical operational levels and the race to secure supplies will intensify. If that happens, he said, “a return above $100 will be imminent.”

“It is crucial to reopen the strait as soon as possible, in order to alleviate supply shortages and, consequently, inflationary pressure,” Varga added.

Inflation is rising

Economic data began to show the broader impact of the war beyond financial markets.

As the war keeps energy costs high, inflation data in various major economies has begun to show rising prices, fueled by a jump in oil, gas, jet fuel and gasoline prices.

In the US, the consumer price index reached an annual rate of 3.8 percent in April, the highest level in almost three years.

Reduced energy supplies from the Middle East have been the main driver of rising inflation, although sharp jumps in prices have prompted some governments, including Germany and India, to intervene.

Paul Surguy, managing director of Kingswood Group, wondered if markets had become “collectively numb to global warfare”.

“Are we witnessing, if not the return of the TACO trade, then simply a general apathy towards constant policy changes from the White House?” he said.

“As for the first, I would hope not for humanity’s sake. As for the second, we’ve seen this play before – the strong market moves at the start of the trade debate were excruciating, but as time went on, the tariff changes may not have even registered on market screens.”

“What we’re seeing is that US war support is at an all-time low, military funding is at an all-time high, and both sides are undoubtedly looking for a face-saving exit. That, more than the current situation on the ground, is likely to affect the longer-term price of oil. Nobody wants to be here in six months.”